When you pick up a prescription at the pharmacy, you might not think about why your $50 brand-name pill suddenly costs $10 - or why it’s gone completely off your plan. The reason? Your employer’s health plan is using a system called a formulary - and it’s pushing you toward generics. This isn’t random. It’s a calculated move to save money, and it affects every prescription you fill.

What Exactly Is a Formulary?

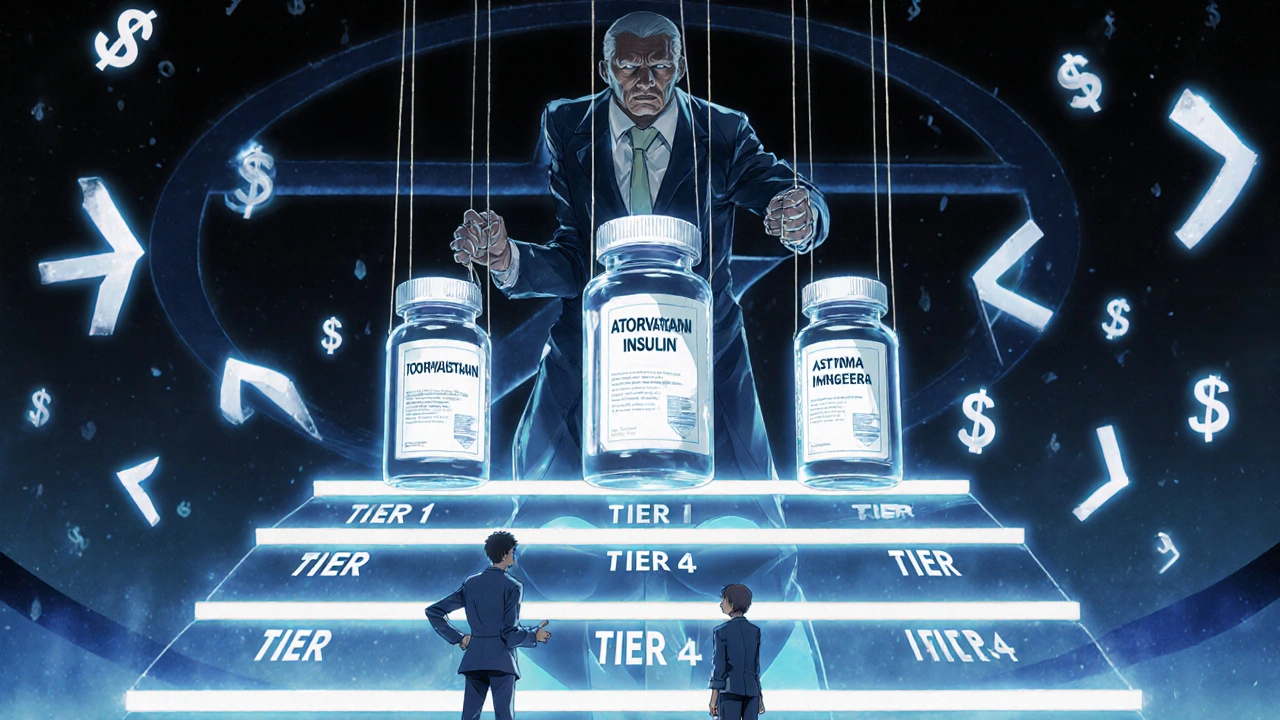

A formulary is a list of drugs your health plan covers. But it’s not just a simple catalog. It’s split into tiers, each with different out-of-pocket costs. Tier 1 is almost always generics - the cheapest option. Tier 2 is preferred brand-name drugs. Tier 3 is non-preferred brands. And Tier 4? That’s for specialty drugs - think biologics for rheumatoid arthritis or insulin pumps - and those can cost hundreds per month.The goal? Get you on the lowest-cost drug that works. And for most conditions, that’s a generic. The FDA says generic drugs are just as safe and effective as their brand-name versions. They contain the same active ingredients, work the same way, and go through the same strict approval process. The only difference? They don’t spend millions on TV ads or clinical trials. That’s why they’re 80-85% cheaper.

Why Employers Push Generics - And How Much They Save

Employers aren’t doing this out of charity. It’s about survival. Prescription drug costs have been climbing for years. In 2023, generic medications saved the U.S. healthcare system over $150 billion annually - that’s $3 billion every week, according to Schauer Group. For a company with 500 employees, switching even half their prescriptions to generics can cut annual drug spending by tens of thousands of dollars.Most large employers (99%, according to Kaiser Family Foundation) offer prescription coverage. But how they structure it varies. Many use tiered copays: $10 for generics, $40 for preferred brands, $75 for non-preferred. When a brand-name drug gets a generic version - say, the cholesterol drug atorvastatin - the pharmacy benefit manager (PBM) automatically moves the brand to Tier 4 and the generic to Tier 1. Suddenly, staying on the brand costs you $65 more per fill. That’s not a coincidence. It’s a financial nudge.

Who Controls Your Drug List? Meet the PBMs

You might not know it, but your drug coverage is managed by a handful of giant middlemen called Pharmacy Benefit Managers - or PBMs. The big three: OptumRx, CVS Caremark, and Express Scripts. Together, they control access to prescriptions for most Americans with employer-based insurance.These companies don’t just decide which drugs are covered. They decide which ones get kicked off the list entirely. In January 2024, each of these three PBMs removed over 600 drugs from their formularies. That’s more than 1,800 drugs gone in one month. Why? To pressure drugmakers into offering bigger discounts. If a manufacturer won’t give a deep enough rebate, the PBM drops the drug. No coverage. No exceptions - unless you fight for one.

Here’s the catch: the savings from these rebates don’t always reach you. PBMs use a pricing trick called gross-to-net (GTN). A drug might have a list price of $100, but after rebates and discounts, the PBM pays only $45. That 55% gap? That’s the GTN spread, according to KPMG. The PBM pockets some of that difference. So even though the system saves billions, you might still pay full price for a brand-name drug - because the discount went to the middleman, not your pocket.

What Happens When Your Drug Gets Removed?

Imagine you’ve been taking a brand-name asthma inhaler for years. It works. You’re stable. Then one day, your plan says it’s no longer covered. The reason? The PBM dropped it because the manufacturer refused to cut prices. Now you’re stuck: pay $300 out of pocket, switch to a generic alternative, or file an exception request.Exception requests aren’t easy. You need a letter from your doctor proving the brand is medically necessary - and even then, approval isn’t guaranteed. Some plans require you to try cheaper alternatives first. This is called step therapy. It’s legal. It’s common. And it can delay your treatment.

Employers are starting to notice the fallout. Some are adding care managers - real people who help employees navigate these roadblocks. HealthOptions.org, for example, assigns care managers to help people find affordable alternatives or get prior authorizations. But not every employer offers this. If yours doesn’t, you’re on your own.

How to Navigate Your Plan - Without Getting Stuck

You don’t have to guess what’s covered. Here’s how to take control:- Check your insurer’s website. Look for your plan’s formulary. Search for your medication by name. It’ll show you the tier and copay.

- Read your Summary of Benefits and Coverage (SBC). It’s a plain-language document your employer must give you. It breaks down drug costs by tier.

- Call your insurer. Ask: “Is there a generic version of this drug? If not, why not?”

- Ask your pharmacist. They often know about alternatives before your doctor does.

- Set up alerts. Formularies change without notice. If your drug gets removed, you won’t get a letter. You’ll find out at the counter.

Also, ask your employer if they offer a Price Assure Program or similar initiative. These programs automatically apply discounts to generics when you fill prescriptions at in-network pharmacies. You don’t have to do anything - the savings are built in.

Why You Should Consider Generics - Even If You’re Skeptical

Many people worry generics aren’t as good. That’s a myth. The FDA requires them to be bioequivalent - meaning they work the same way in your body, within a 3-5% margin. Millions of people take generics every day with zero issues. In fact, 90% of all prescriptions filled in the U.S. are generics.And the savings add up fast. Take a diabetes medication like metformin. The brand version might cost $120 a month. The generic? $4. That’s $1,400 saved per year - just for one pill. Multiply that by five medications, and you’re talking $7,000 in annual savings. That’s a vacation. A new tire. An emergency fund.

Employers know this. That’s why they’re pushing generics harder than ever. Some even offer bonus incentives - like $0 copays for generics - to encourage switching.

The Bigger Picture: Is This System Fair?

There’s a disconnect. The system saves billions. PBMs profit. Employers save money. But employees? Sometimes they’re left paying more for the same drug - or going without because the only option left is too expensive.Experts like Scott Glovsky point out that without transparency, the system becomes a black box. You don’t know why a drug was removed. You don’t know how much of the rebate you’re missing out on. And you don’t know when the next change will hit.

That’s why education matters. Employers need to do more than send a one-time email. They need ongoing conversations - through payroll stuffers, team meetings, even text reminders. Many employees would switch to generics if they understood how safe and affordable they are. But too many are scared of change.

What’s Next?

The trend won’t reverse. PBMs will keep using formulary exclusions as leverage. Employers will keep pushing generics. Drugmakers will keep raising list prices - hoping to offset lost sales.What can you do? Stay informed. Check your formulary every time you refill a prescription. Ask questions. Don’t assume your plan hasn’t changed. And if your drug disappears, don’t give up. Talk to your doctor. Ask about alternatives. File for an exception if needed.

This isn’t about fighting the system. It’s about understanding it. The rules are complex, but they’re not impossible to navigate. The more you know, the less power the system has over you.

Are generic drugs really as good as brand-name drugs?

Yes. The FDA requires generic drugs to have the same active ingredients, strength, dosage form, and route of administration as the brand-name version. They must also prove they work the same way in your body. Over 90% of prescriptions in the U.S. are generics - and they’re used safely every day by millions.

Why did my prescription suddenly stop being covered?

Your plan’s Pharmacy Benefit Manager (PBM) likely removed the drug from its formulary. This happens when the drugmaker doesn’t offer a big enough discount. PBMs do this to pressure companies into lowering prices. Changes can happen without notice, so always check your formulary before refilling.

Can I get my brand-name drug covered if I really need it?

Yes - but it’s not automatic. You’ll need a letter from your doctor explaining why the generic won’t work for you. This is called a medical necessity exception. Some plans require you to try cheaper alternatives first. Approval isn’t guaranteed, but it’s worth asking.

Why is my generic drug still expensive?

Even generics can cost more if your plan doesn’t cover them at Tier 1, or if your pharmacy isn’t in-network. Also, some PBMs don’t pass rebates to consumers - so while the system saves money, you might still pay more than expected. Always compare prices at different pharmacies - sometimes cash prices are lower than your copay.

What’s the difference between a preferred and non-preferred brand-name drug?

Preferred brand-name drugs are on your plan’s formulary and have better pricing - usually because the drugmaker gave the PBM a bigger rebate. Non-preferred brands aren’t favored, so your out-of-pocket cost is higher. Often, switching to a preferred brand can cut your cost in half.

How often do formularies change?

All the time. New generics enter the market monthly. PBMs update their lists quarterly or even monthly. Some changes happen overnight. That’s why checking your formulary before each refill is critical. Don’t wait until you’re at the pharmacy.

Should I switch to a generic even if I’ve been on a brand for years?

Talk to your doctor first - but in most cases, yes. Generics are proven safe and effective. Millions of people switch without issue. The biggest barrier is fear, not science. If your condition is stable and your doctor agrees, switching can save you hundreds or even thousands per year.

Erika Sta. Maria

November 22, 2025 AT 02:51So let me get this straight-your ‘savings’ are just PBMs pocketing the difference while you’re left paying $65 more for a pill your body’s been used to for 12 years? 🤯 And you call this ‘healthcare’? This isn’t capitalism-it’s a slow-motion hostage situation with a pharmacy receipt.

Steve Harris

November 22, 2025 AT 03:51For anyone new to this: generics are absolutely safe. I’m a pharmacist with 18 years in the field, and I’ve seen zero clinical difference between brand and generic insulin, statins, or even antidepressants. The FDA’s bioequivalence standards are brutal. If your doctor says ‘switch,’ they’re not gambling-they’re saving you money without sacrificing efficacy. Trust the science, not the fear.

Michael Marrale

November 23, 2025 AT 12:13Wait… so the same companies that run your drug coverage also control the data on what drugs get dropped? And they’re owned by the same big pharma conglomerates? Hmm. Interesting. I mean, why would they ever do something that hurts patients? Oh right-because they’re owned by the same people who make the brand-name drugs they’re forcing you off of. It’s all connected. The system isn’t broken-it’s designed this way. You’re not a patient. You’re a revenue stream.

David vaughan

November 23, 2025 AT 19:57Just wanted to say… I switched my blood pressure med to generic last year… and I’ve saved $1,200. I didn’t even notice a difference. Honestly? I felt kinda dumb for being scared. Also, my pharmacist told me to check GoodRx-it’s wild how much cheaper cash prices can be than your copay. 🙏

David Cusack

November 23, 2025 AT 23:56One must acknowledge that the formulary system is a marvel of economic rationalism-though its implementation reveals a grotesque dissonance between efficiency and human dignity. The PBM, as a quasi-privatized arbiter of pharmaceutical access, operates in a vacuum of accountability. One wonders whether the FDA’s bioequivalence metrics are sufficient to account for psychosomatic variables in patient adherence… or if we’ve simply outsourced ethics to actuarial tables.

Elaina Cronin

November 24, 2025 AT 03:25This is unconscionable. People are dying because they can’t afford their meds-and you’re all sitting here debating ‘formularies’ like it’s a boardroom meeting? This isn’t ‘cost-cutting.’ It’s medical rationing disguised as capitalism. If your employer cares more about quarterly profits than your life, find a new job. Or better yet-demand universal healthcare. This system is not just broken-it’s cruel.

Willie Doherty

November 25, 2025 AT 08:43Let’s analyze the data: 90% of prescriptions are generics. That’s 3.6 billion prescriptions annually. If the average savings per generic is $50, that’s $180 billion in aggregate savings. But PBMs retain 25–40% of rebates-so $45–72 billion is siphoned off. Employers save $30–50 billion. Patients? Less than $10 billion in direct savings. The math doesn’t lie: the system is designed to extract, not to heal.

Darragh McNulty

November 27, 2025 AT 01:47Hey everyone-just a quick heads-up 🙌 If you’re on a brand-name drug and it got dropped, don’t panic. Call your doctor, ask for a prior auth, and check GoodRx or SingleCare. I saved $200/month on my asthma inhaler by switching to a generic and using a coupon. You got this 💪

Cooper Long

November 27, 2025 AT 06:32Generics are not inferior. They are identical. The FDA does not approve them lightly. In fact, many generics are manufactured in the same facilities as brand-name drugs. The difference is marketing, not medicine. The fear is manufactured. The savings are real.

Sheldon Bazinga

November 28, 2025 AT 15:02Typical US healthcare scam. First they make you pay $500 for a pill, then they say ‘oh btw we’re gonna make you pay $5 for the same pill but it’s called something else’-like a magic trick where the rabbit is your dignity. Meanwhile, the Chinese factories making these generics are probably paid less than minimum wage. Who’s really winning here? Nobody. Just corporations and their tax havens.

Sandi Moon

November 28, 2025 AT 21:40Of course the PBMs are the real villains. But let’s not pretend this is uniquely American. In the UK, the NHS has been doing this for decades-rationing drugs, pushing generics, denying access based on cost-effectiveness. The difference? At least they’re honest about it. Here? We pretend we’re helping while quietly starving patients. It’s not capitalism. It’s fascism with a pharmacy receipt.

Kartik Singhal

November 29, 2025 AT 02:35Bro… you think this is bad? In India, generics are the ONLY option. We’ve been using them for 30 years. My uncle takes 7 different generics for diabetes, hypertension, and arthritis. He’s 82. Still walks 5km a day. No side effects. No drama. The fear is cultural, not medical. Also, if you can’t afford your meds, you’re already in the wrong country. 😎

Logan Romine

November 30, 2025 AT 03:50So… we’re supposed to be grateful that our employer is saving money by making us risk our health? 😏 Funny how ‘cost-effective’ always means ‘you pay more, you suffer more, you shut up.’ Meanwhile, the CEO’s health plan probably covers IV vitamin drips and cryotherapy. But hey-‘generics are just as good.’ Right. 😌